Trump Is Extending Obamacare Subsidies? If you’re one of the millions of Americans who count on Obamacare subsidies to keep health insurance affordable, you’ve probably heard the buzz: President Trump is reportedly considering a plan to extend those subsidies for two more years. But don’t get too excited just yet—this isn’t a done deal, and there are some major twists and turns that could change everything for your wallet and your coverage. Let’s break it down in plain English, so whether you’re a parent, a small business owner, or just trying to figure out your health plan, you’ll know exactly what’s going on.

Trump Is Extending Obamacare Subsidies?

Trump’s move to extend Obamacare subsidies is a game-changer, but it’s far from certain. If Congress passes an extension, millions of Americans will keep affordable coverage. If not, premiums could skyrocket and coverage could vanish for many. Stay tuned, check your eligibility, and make a plan before the deadline hits.

| What’s Happening? | Why It Matters | What You Should Know |

|---|---|---|

| Trump is weighing a proposal to extend ACA subsidies for two years | Millions could avoid huge premium hikes if subsidies continue | The plan is not final and faces Republican pushback |

| Current subsidies expire December 31, 2025 | Without an extension, average premiums could more than double | Enrollees with incomes above 400% of the poverty level may lose all help |

| The new proposal may cap eligibility at 700% of poverty and require minimum premiums | Could affect middle-income families and eliminate zero-premium plans | Check your eligibility and plan options before open enrollment ends |

| Extension could cost $60 billion over two years | Taxpayers and lawmakers are debating the cost | Experts say coverage could drop by millions if subsidies expire. |

| Official Source: Healthcare.gov |

What Are Obamacare Subsidies?

Obamacare subsidies, officially known as the Affordable Care Act (ACA) premium tax credits, are government payments that help lower your monthly health insurance bill if you buy a plan through the Health Insurance Marketplace. These subsidies are based on your income and household size. In 2025, if your income is between 100% and 400% of the federal poverty level (FPL), you qualify for help paying for your premiums.

For example:

- A single person earning $15,060 to $60,240 in 2025 may get a subsidy.

- A family of four earning $31,200 to $124,800 could also qualify.

Thanks to these subsidies, over 24 million Americans enrolled in Marketplace plans for 2025—many paying less than $10 a month for coverage.

Why Are Subsidies About to Expire?

The current enhanced subsidies were extended by the Inflation Reduction Act through the end of 2025. After that, unless Congress acts, the rules snap back to their pre-2021 levels, which means:

- The income cap for subsidies returns to 400% of the FPL.

- Premiums could skyrocket, especially for middle-income families.

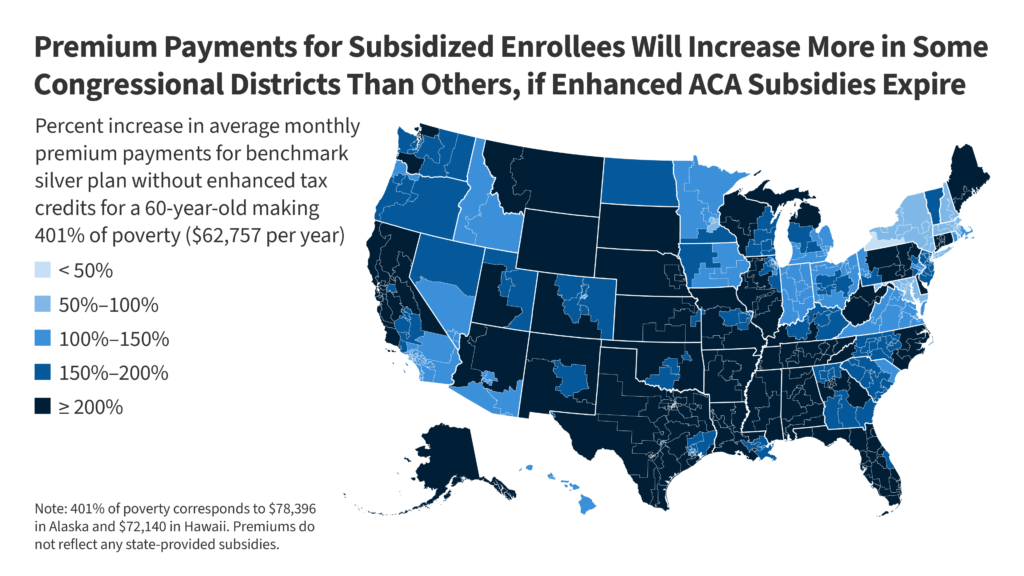

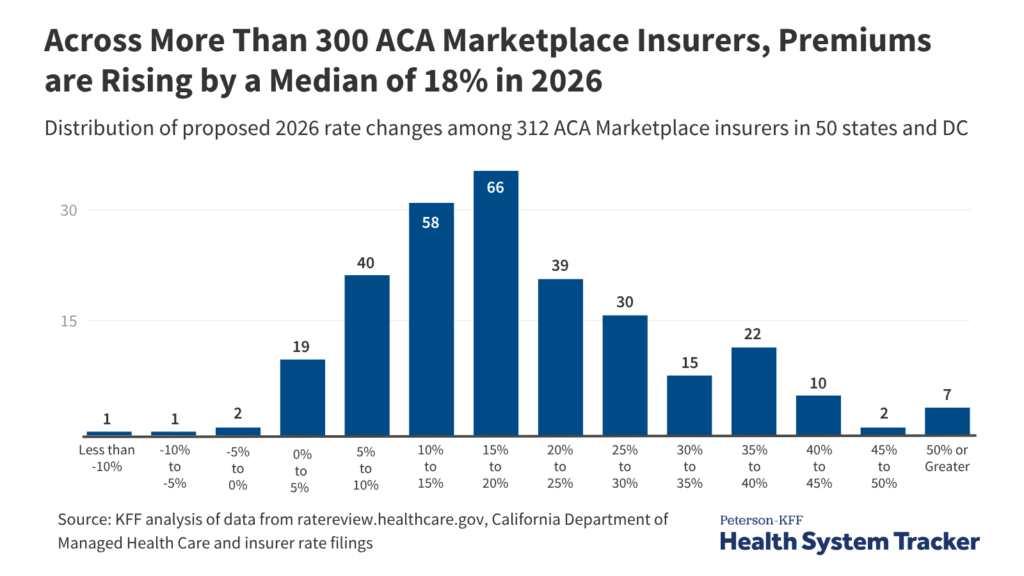

Experts estimate that if subsidies expire, average premiums will more than double for subsidized enrollees—from about $888 a year to $1,904. That’s a 114% increase for many families.

Trump Is Extending Obamacare Subsidies?

Here’s the twist: President Trump, who has long called Obamacare a “disaster,” is now open to extending the subsidies for two years. But there’s a catch—his proposal would:

- Cap eligibility at 700% of the poverty level (higher than the current 400% cap).

- Require enrollees to pay a minimum monthly premium, possibly eliminating zero-premium plans for the lowest-income families.

This move is meant to prevent a wave of premium hikes and coverage losses, but it’s controversial. Some Republicans worry it’s too much government spending, while Democrats want a straightforward extension without new restrictions.

State-by-State Impact of Trump Is Extending Obamacare Subsidies?

The impact of subsidy changes varies by state. States with higher concentrations of ACA enrollees—like Texas, Florida, Georgia, and North Carolina—could see the biggest enrollment drops if subsidies expire. In some states, enrollment is already down:

- Washington state has seen a 21% increase in disenrollments.

- California’s enrollment dropped 33% compared to last year.

- Pennsylvania reports two existing enrollees dropping coverage for every new sign-up.

Alternatives If Subsidies Expire

If Congress fails to extend subsidies, you still have options:

- Short-term health plans: These are usually cheaper but offer limited coverage and aren’t required to cover pre-existing conditions.

- Health-sharing ministries: Faith-based groups that pool money to help members pay medical bills.

- Medicaid: If your income is very low, you may qualify for Medicaid instead.

Experts advise signing up for Marketplace coverage by the December 15 deadline, even if you’re unsure about the subsidy extension. If premiums become unaffordable, you can always drop your plan at the end of the month, but you won’t be able to re-enroll until next year’s open enrollment.

Impact on Families and Workers

The subsidy cliff—where benefits sharply drop as income rises—can create major problems for families and workers. For example:

- A family earning just above 400% of the poverty level could lose all subsidies and face a massive premium hike.

- Workers with employer-sponsored insurance may be worse off than those who get subsidies through the Marketplace, especially if their employer plan is expensive or offers poor coverage.

- The Congressional Budget Office (CBO) estimates that if subsidies expire, about 4 million Americans could lose coverage over the next decade, and families could see their healthcare costs rise by thousands of dollars per year.

Impact on Employers and the Economy

The end of enhanced subsidies could also hit employers and the economy:

- Many small businesses rely on employees getting subsidized coverage through the Marketplace, allowing them to pay higher wages instead of offering expensive health plans.

- If subsidies expire, employers may have to spend more on health benefits or risk losing workers to jobs that offer better coverage.

- The CBO also projects that the loss of subsidies could result in nearly 5 million job losses and a significant increase in the number of uninsured Americans, which could strain hospitals and raise costs for everyone.

Legislative Process and What’s Next

Congress must act before December 31, 2025, to extend the subsidies. The process is complex and involves negotiations between Democrats, Republicans, and the White House. Bipartisan groups in Congress have floated several proposals, including:

- A two-year extension with new eligibility rules and fraud protections.

- Converting subsidies into direct payments to consumers.

- Cracking down on “ghost beneficiaries” and ensuring only eligible people receive help.

President Trump has not yet made a final decision, but the White House is circulating a draft proposal and pushing for a deal before the end of the year.

What Should You Do Now?

- Check your eligibility for subsidies using the official calculator on Healthcare.gov

- Review your plan options before open enrollment ends (usually December 15 for 2026 coverage).

- Stay informed—the situation is fluid, and Congress could pass a new law at any time.

- Consider alternative coverage if you’re close to the income cutoff and might lose help.

- Talk to a broker or navigator if you need help comparing plans or understanding your options.

$550K Mistake Still Haunts Richmond: Retirement System Keeps Paying Dead Retirees, Audit Reveals

U.S. Stock Futures Surge as Wall Street Bets Big on Thanksgiving Week and Holiday Sales

Social Security Benefits in December 2025; Check SSI and SSDI deposit schedule