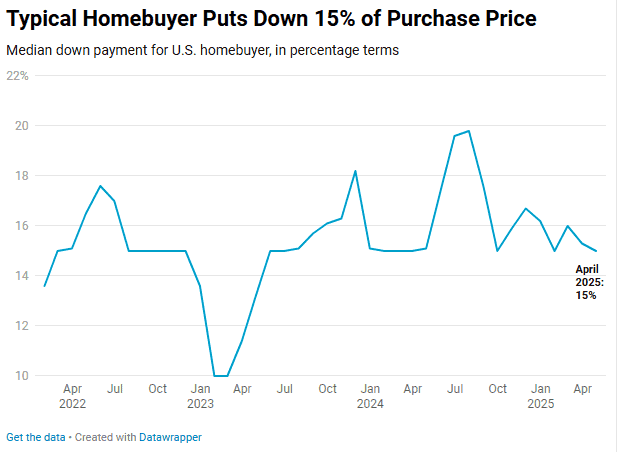

Average Down Payment Soars Past $63K: Buying a home in America has always been a milestone — a dream wrapped up in white picket fences, backyard barbecues, and the smell of fresh paint. But for today’s buyers, that dream comes with a hefty price tag. According to Nasdaq and Redfin, the average U.S. down payment just broke a record — soaring past $63,000. That’s about the cost of a new Tesla Model Y or two years of tuition at an Ivy League university. And with mortgage rates hovering near 7%, many families feel like homeownership is slipping out of reach. But here’s the twist — while most people are tightening their belts, states like Texas, California, and Florida are quietly stepping in with new and expanded down payment aid programs to keep the dream alive.

Average Down Payment Soars Past $63K

The average down payment soaring past $63,000 is both a warning and a challenge. It signals how tough the U.S. housing market has become — but also how innovative solutions are emerging. Programs in Texas, California, and Florida show that smart policy can turn renters into homeowners, strengthen communities, and make the American Dream more accessible again. Whether you’re a teacher in Dallas, a nurse in Sacramento, or a small business owner in Tampa, the door to homeownership isn’t locked — you just need the right key.

| Topic | Details |

|---|---|

| Average U.S. Down Payment (2025) | $63,188 (up 7.5% YoY) |

| Average % of Home Price | 16–19% of median home price |

| Median U.S. Home Price | $420,800 (Q3 2025) |

| Top States Offering Aid | Texas, California, Florida |

| Types of Assistance | Grants, forgivable loans, shared appreciation programs |

| Eligibility Range | First-time & moderate-income buyers |

| Mortgage Rate (Nov 2025) | Around 6.8% average |

| Typical Household Income to Buy Median Home | $110,000+ in most metros |

Why Average Down Payment Soars Past $63K?

It’s no secret that the cost of living has climbed, but the housing market is in its own league.

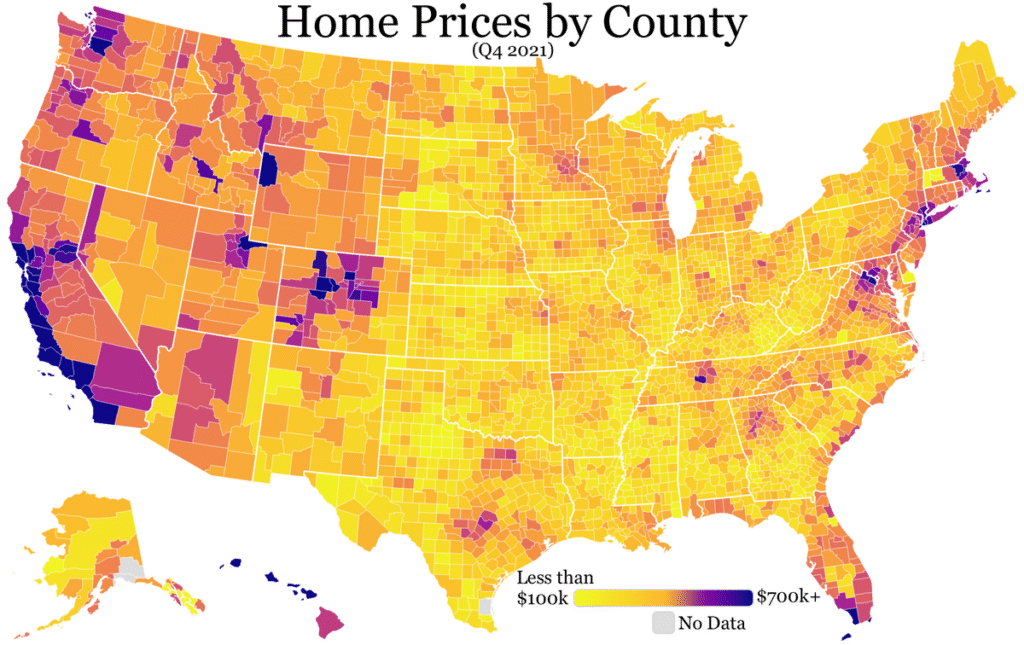

The median home price in the U.S. hit $420,800, marking a 30% rise since 2019. Combine that with inflation, higher interest rates, and record-low housing supply, and it’s easy to see why homebuyers are being squeezed.

So, what’s driving this surge?

- Tighter lending standards: Banks want security. Since the 2008 crash, lenders demand higher down payments from buyers to reduce risk.

- Fierce competition: With limited listings, buyers are bidding higher and offering larger cash down payments to win homes.

- Investor influence: Wall Street-backed firms and cash buyers continue to dominate the market, forcing everyday families to put more money down to compete.

- High mortgage rates: When rates rise, sellers lower concessions — pushing more costs onto buyers upfront.

Even in smaller towns, where homes used to be more affordable, down payments are climbing fast. ATTOM Data Solutions reported that in mid-2025, buyers in cities like Dallas, Orlando, and San Diego were putting down more than $60,000 on average.

The Silver Lining: State Aid Is Expanding

Thankfully, some states aren’t leaving their residents hanging. Texas, California, and Florida — three of the nation’s hottest real estate markets — have quietly expanded or relaunched down payment assistance (DPA) programs aimed at first-time and middle-income buyers.

These programs can mean the difference between dreaming of a home and owning one.

Texas: “Homes for Texas Heroes” & “Home Sweet Texas”

The Texas State Affordable Housing Corporation (TSAHC) runs two flagship programs:

- Homes for Texas Heroes — targeted at teachers, firefighters, police, EMS, veterans, and health professionals.

- Home Sweet Texas — open to low-to-moderate-income Texans.

Program Highlights:

- Grants and 0%-interest loans covering up to 5% of the mortgage amount.

- Forgivable after living in the home for a set period (usually three years).

- Can be combined with a Mortgage Credit Certificate (MCC) for federal tax savings.

Example:

A Dallas paramedic buying a $300,000 home can receive $15,000 in grant aid. Add an MCC, and they could save another $2,000–$3,000 annually on taxes.

California: The Dream For All Program

California’s CalHFA Dream For All program has made national headlines for its shared appreciation loans.

Here’s how it works:

- The state contributes up to 20% of your home’s price as a second loan.

- You repay the same percentage of the home’s appreciation when you sell or refinance.

- No monthly payments while you own the home.

Example:

If you buy a $500,000 home with $100,000 from CalHFA and sell it later for $700,000, you repay $100,000 + 20% of the gain ($40,000).

This program was so popular that the initial funding ($300 million) ran out in just 11 days in 2023. In 2025, California reintroduced it with new funding and adjusted income limits to reach more working families.

Florida: The Hometown Heroes Expansion

Florida’s Hometown Heroes Housing Program initially focused on first responders and teachers. But in 2024, the state opened it to nearly all employed residents.

Key Benefits:

- Up to $35,000 in down payment and closing cost assistance.

- 0% interest, deferred-payment loans (no monthly payments).

- Funds due only when you sell, refinance, or stop using the property as your main home.

With home prices in Miami topping $600,000, this program is a lifeline for working professionals trying to stay near their jobs.

How These Programs Work in Practice?

Let’s put some numbers on it.

Imagine you’re buying a $400,000 home in Texas with a 3% down payment and $8,000 in closing costs.

That’s roughly $20,000 out of pocket.

If you qualify for a 5% TSAHC grant ($20,000), your upfront cost could drop to almost zero.

That’s real relief for families who’ve been renting for years because saving that much cash felt impossible.

What Buyers Need to Know About Average Down Payment Soars Past $63K?

While these programs can open doors, they’re not a free ride. You’ll still need to meet certain requirements:

- Credit score: Usually 620 or higher.

- Income limits: Vary by county; most cap around 80%–120% of median income.

- Primary residence: You must live in the home full-time.

- Education course: Most states require a HUD-approved homebuyer class.

These safeguards ensure the funds go to responsible, informed buyers who’ll actually benefit.

Practical Tips to Qualify and Succeed

- Start early: Many programs operate on limited budgets. Once funds run out, applications close.

- Shop lenders: Not every bank offers DPA-friendly loans. Look for approved lenders listed on official sites.

- Stack assistance: Some cities (like Austin or Los Angeles) have local grants you can combine with state aid.

- Get pre-approved: Know your price range and lock in rates before bidding wars heat up.

- Work with professionals: A licensed real estate agent familiar with DPA programs can guide you through paperwork and deadlines.

Expert Perspective: Economists Weigh In

Housing economists say these programs play a crucial role in promoting financial inclusion.

“Down-payment aid isn’t a handout; it’s an investment in stable communities,” explains Daryl Fairweather, Chief Economist at Redfin.

“When middle-income buyers can finally afford homes, we see higher local spending, better schools, and stronger tax bases.”

But there’s a catch. Some analysts worry that too much aid could inflate prices further if demand spikes without new housing supply. Experts suggest pairing financial aid with zoning reforms and new construction incentives.

How to Apply for Average Down Payment Soars Past $63K(Step-by-Step Guide)?

- Visit your state housing agency’s website.

Example: TSAHC, CalHFA, Florida Housing. - Check program eligibility.

Review income, credit, and home price limits. - Complete a homebuyer education course.

Take it online through HUD-approved providers. - Find an approved lender.

Choose one familiar with your state’s program. - Get pre-approved for a loan.

Lenders will calculate how much assistance you qualify for. - Submit documents and lock your funds.

Timing matters — assistance funds can disappear quickly. - Close on your new home.

Once approved, the assistance applies directly at closing to reduce your out-of-pocket costs.

SNAP benefits Payment Date in December 2025; Check Payment Amount & State Wise Eligibility

Trump Is Extending Obamacare Subsidies? Inside the Surprising Twist That’s Changing Everything