2026 Social Security Check May Shrink: Are you worried about your 2026 Social Security check? You’re not alone! Millions of Americans are bracing themselves for higher Medicare premiums, which will cut into the much-anticipated cost-of-living boost. This guide breaks down what’s changing, how much you’ll actually get, and how to stay ahead of the curve—explained in a way anyone from your 10-year-old grandkid to seasoned financial pros can understand.

2026 Social Security Check May Shrink

Your 2026 Social Security cost-of-living increase is real, but for most retirees and seniors, a hefty chunk of that “raise” goes right back into higher Medicare premiums. Planning and reviewing your benefits now can help offset surprises when checks go out in January. Want to keep more in your wallet? Shop plans, review your income status, and seek out assistance if you qualify.

| Feature | 2025 Amount | 2026 Amount | Change |

|---|---|---|---|

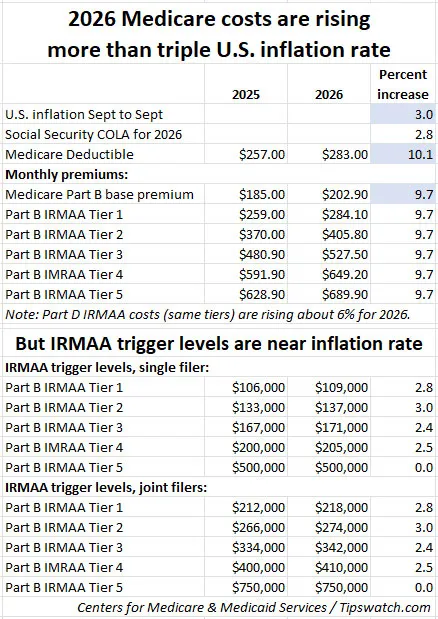

| Medicare Part B Premium (Standard) | $185.00 | $202.90 | +$17.90 (9.7%) |

| Medicare Part B Deductible | $257 | $283 | +$26 |

| Social Security COLA (Average Monthly Increase) | ~$56 | See 2026 COLA | ~2.8% COLA |

| Income Threshold for Higher Premiums (Single/Joint Filers) | $109,000/$218,000 | $109,000/$218,000 | No change |

| Hold Harmless Rule Protection | Yes (for most) | Yes (for most) | Slight expansion |

| Medicare Part D Out-of-Pocket Cap | $2,000 | $2,100 | +$100 |

| Medicare Advantage Enrollment | 34.9 million | 34 million | Slight decrease |

What’s the Deal With Social Security and Medicare in 2026?

Social Security checks will get a boost thanks to COLA (Cost-of-Living Adjustment), but for millions of Americans, the real payday is gonna look a lot leaner. That’s because Medicare Part B premiums are set to jump by almost $18 a month—right out of your Social Security payment. Basically, Medicare is taking a bigger bite from your check before you even see it.

Premiums are rising for a reason: Medicare costs are going up, hospital stays and outpatient procedures cost more, and the wave of Baby Boomers turning 65 isn’t slowing down anytime soon. In fact, 2026 is seeing the highest premium hike in four years—making it the second-largest dollar jump ever for Part B.

Breaking Down the Numbers

Social Security’s “Raise”… With a Catch

- The 2026 Social Security COLA is about 2.8%. For the average retiree, that’s roughly $56 more per month.

- But the Medicare Part B premium jumps to $202.90—almost $18 higher than last year.

- That means nearly one-third of your Social Security “raise” goes straight to Medicare before hitting your bank account.

Here’s a real-world example:

Let’s say you got $2,015/month from Social Security in 2025.

- With COLA, your 2026 check jumps to $2,071/month (about a $56 bump).

- BUT…the new Medicare premium is $202.90, compared to $185 in 2025.

- So, your actual net increase is closer to $38/month after Medicare takes its cut.

Premium Tiers: High Earners Pay More

Medicare Part B premiums aren’t one-size-fits-all. If your income is higher, you’ll pay a lot more:

- Single filers over $109,000 or married couples over $218,000 face bigger premiums.

- The highest earners (singles $500,000+, couples $750,000+) will pay up to $689.90 per month for Part B!

- Income-related adjustments are calculated based on your modified adjusted gross income (MAGI) from two years prior.

Other Costs to Watch

- Part B Deductible: Jumps from $257 to $283 in 2026.

- Part A Deductible: Up to $1,736 per hospital stay (from $1,676).

- Medicare Advantage & Part D: Some insurer plans are seeing fewer options, higher premiums, and rising out-of-pocket limits, especially for prescriptions and specialist care.

Who Gets Pinched the Hardest With 2026 Social Security Check May Shrink?

- Middle-income retirees who don’t qualify for low-income savings programs.

- High-income seniors who cross Medicare’s income thresholds.

- People on Medicare Advantage plans in 2026 may find fewer $0 premium options—some counties are down to no Advantage plans at all, especially after big insurers like Elevance and Blue Cross exit certain regions.

Good News: Most people still have a choice of plans (about 32 options on average), but you’ll need to shop harder this year.

What Can You Do About It? Practical Steps

1. Review your Social Security and Medicare mail.

Expect official notices by mail and watch for updated premium and benefit notices from the SSA and Medicare.

2. Compare all your Medicare plans during open enrollment (ends Dec 7th).

Don’t set it and forget it. You might save by switching plans based on your needs.

3. Understand income-related premiums.

If your income has dropped, report it to Social Security; you could be eligible for lower premiums.

4. Apply for assistance programs.

Low-income beneficiaries should ask about Medicare Savings Programs and Extra Help for prescription costs

- Qualified Medicare Beneficiary (QMB): Covers Part A & B premiums, deductibles, and coinsurance for those at or below 100% of the federal poverty level

- Specified Low-Income Medicare Beneficiary (SLMB): Covers Part B premiums for those between 100% and 120% of the poverty level

- Qualifying Individual (QI): Covers Part B premiums for those between 120% and 135% of the poverty level.

5. Takeout coverage for gaps.

Medicare doesn’t pay for everything, so review supplemental (Medigap) plans to limit your out-of-pocket risk.

6. Consult a professional.

A financial advisor or SHIP counselor can help you see the whole picture and avoid surprises.

Hold Harmless Rule: What It Means for You

The hold harmless rule protects most Social Security recipients from seeing their checks drop due to higher Medicare Part B premiums. If your Social Security benefit is low enough (around $600 or less), this rule ensures your check won’t shrink even if premiums go up. However, this rule only applies to Part B premiums deducted from Social Security—not Part D or Advantage premiums, and not if you pay Medicare directly.

Medicare Advantage & Prescription Drug Changes in 2026

- Medicare Advantage plans: Some insurers are exiting certain markets, and some plans are being discontinued. If you’re affected, you’ll get a notice by October and have until December 7th to switch. If you miss the deadline, you may have a special enrollment window until the end of February 2026.ryoutube

- Prescription drugs: 2026 brings lower prices on 10 popular high-cost drugs, and the drug spending cap is rising. This could save beneficiaries about $1.5 billion in out-of-pocket costs.

Medicare Part D Prescription Drug Coverage in 2026

Medicare Part D is getting some major upgrades in 2026. The most important change is the out-of-pocket spending cap, which rises from $2,000 in 2025 to $2,100 in 2026. Once you hit this cap, your plan covers 100% of your drug costs for the rest of the year, no matter what you need. This cap applies to both stand-alone Part D plans and prescription coverage included in Medicare Advantage plans.

- The maximum deductible for Part D plans is now $615, up from $590 in 2025.

- For many, Part D premiums are actually decreasing in 2026, especially in certain states.

- Medicare is negotiating prices for 10 widely used drugs, which could mean discounts of 38% to 79% on medications like Eliquis, Xarelto, Januvia, Jardiance, and Farxiga.

Medigap (Medicare Supplement) Plans: What’s Changing?

If you have a Medigap plan, here’s what’s new in 2026:

- Medigap Plan C and high-deductible Plan F are no longer available for people newly eligible for Medicare in 2026.

- The deductible for Medigap Plan G is now $2,950, up from $2,870 in 2025.

- Medigap premiums generally rise each year, and switching plans may require medical underwriting unless your current plan is being discontinued.

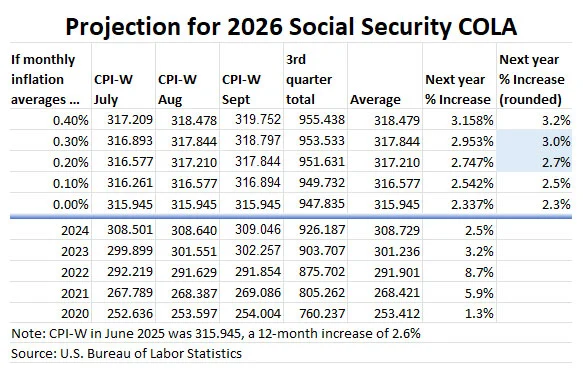

How Social Security COLA Is Calculated?

The 2026 Social Security COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a narrow price index that tracks inflation for certain groups. The formula uses the change in CPI-W from the third quarter of 2024 to the third quarter of 2025. This method tends to overstate inflation slightly, but it ensures that benefits move up with the cost of living.

- The 2026 COLA is 2.8%, raising the average retiree’s monthly benefit from $2,015 to $2,071.

- The maximum taxable earnings for Social Security go up to $184,500 in 2026, from $176,100 in 2025.

- The retirement earnings test also changes, with higher exempt amounts for those under full retirement age ($24,480 in 2026) and those reaching full retirement age ($65,160 in 2026).