2026 Earnings Limit Is Going Up: If you’re one of the millions of Americans receiving Social Security benefits while still clocking in some work hours, here’s good news: the 2026 earnings limit is officially going up. That means retirees can now earn more money without losing a chunk of their monthly benefits. Let’s break it all down in plain English, so whether you’re 30, 60, or 90, you can understand exactly how this helps you. The Social Security Administration (SSA) has confirmed several key updates for 2026 that affect retirees, workers, and future beneficiaries. One of the most talked-about changes? The higher earnings limit — a relief for retirees who want to work part-time or stay active in the job market.

2026 Earnings Limit Is Going Up

The 2026 Social Security changes — especially the higher earnings limit — are a welcome relief for retirees who want to stay in the workforce without being penalized. Combined with a modest COLA increase and better income flexibility, these adjustments help Americans balance work, life, and retirement more effectively. For those nearing retirement, now’s the perfect time to revisit your plan, understand your FRA, and use the tools to make the most of your benefits.

| Topic | Details for 2026 |

|---|---|

| Earnings Limit (Below Full Retirement Age) | $24,480 (up from $23,400 in 2025) |

| Earnings Limit (Year You Reach Full Retirement Age) | $65,160 (up from $62,160 in 2025) |

| Full Retirement Age (FRA) | 66-67, depending on birth year |

| COLA (Cost of Living Adjustment) | Estimated 2.7% increase |

| Wage Base for Social Security Tax | $184,500 (up from $176,200) |

| Medicare Part B Premium (Projected) | $206.50/month |

| Maximum Monthly Benefit at FRA | $4,030/month |

| Social Security Credit Requirement | $1,760 per credit |

What Does the 2026 Earnings Limit Is Going Up Mean?

Think of the earnings limit as the amount you can earn from a job before Social Security starts temporarily withholding some of your benefits. If you haven’t reached your full retirement age (FRA) yet, this rule applies to you. The good news? That limit is getting a nice bump for 2026.

- In 2025, retirees under FRA could earn up to $23,400 without any penalty.

- In 2026, that threshold climbs to $24,480.

That means you can earn an extra $1,080 a year and still keep your full benefits.

If you’re hitting your FRA in 2026, you’re allowed to earn up to $65,160 for the year before any deductions kick in — a jump of $3,000 from 2025.

And once you’re past your full retirement age, there’s no limit on how much you can earn. You could pull in $25,000 or $250,000 — your benefits won’t be reduced a dime.

This bump is particularly significant for the millions of Americans who work part-time after retirement. According to AARP, nearly 35% of Americans aged 65 to 74 are expected to still be working by 2030. The change allows these older workers to stay in the workforce longer, supplementing their income while preserving their Social Security benefits.

How the Earnings Test Works (and Why It’s Not as Scary as It Sounds)?

Many retirees get nervous when they hear that their benefits might be reduced if they earn too much. But here’s the deal: you don’t actually lose that money forever.

Here’s how the math works:

- Before FRA: For every $2 you earn over the limit, Social Security withholds $1 of your benefits.

- During the year you reach FRA: The formula changes — the SSA withholds $1 for every $3 you earn over the higher limit.

- After FRA: No withholdings at all. You can work full-time, part-time, or run your own business freely.

For example, suppose you’re 64 and earn $30,000 in 2026. That’s $5,520 over the limit ($30,000 – $24,480). Social Security would withhold $2,760 ($1 for every $2 earned over). It sounds harsh, but remember: those withheld benefits come back later. Once you hit full retirement age, the SSA recalculates your payments and adjusts your monthly amount upward.

This rule encourages people to keep working while maintaining flexibility. It’s not a punishment — it’s a temporary adjustment.

Why the 2026 Earnings Limit Is Going Up Matters More Than You Think?

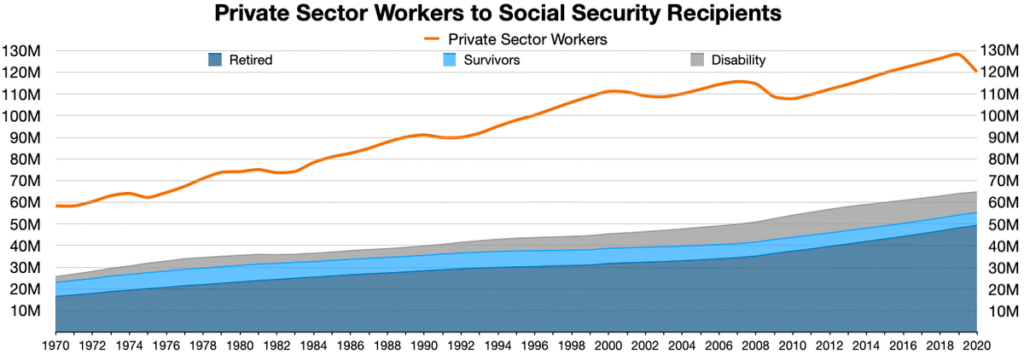

This change comes at a time when inflation, healthcare costs, and housing prices are squeezing retirees hard. The Senior Citizens League (TSCL) reports that nearly 60% of older Americans rely on Social Security for at least half of their income. So, being able to earn more from work without losing benefits can make a meaningful difference.

Let’s say you pick up a part-time gig at Home Depot, drive for Uber, or do consulting work. That extra income can help cover:

- Rising Medicare Part B premiums (projected to hit $206.50/month in 2026)

- Groceries and utilities, which have risen roughly 12% since 2020

- Travel or hobbies that make retirement enjoyable

This flexibility is particularly helpful for early retirees who may not yet qualify for Medicare or those supporting family members. Many Americans now find themselves part of the so-called “sandwich generation” — caring for both aging parents and adult children. A higher earnings limit can ease some of that financial burden.

Cost-of-Living Adjustment (COLA): A Small but Welcome Boost

Alongside the higher earnings limit, the 2026 COLA is expected to rise by about 2.7%, according to TSCL. It’s not massive, but it helps counter rising costs.

Using the average monthly benefit of $2,006.69 (as of July 2025), that means retirees will see an average $54.18 monthly increase — or $650.16 a year.

However, inflation is still a concern. The Federal Reserve expects inflation to hover around 2.4% in 2026, meaning the COLA will roughly keep pace but won’t dramatically increase buying power. Still, when combined with the higher earnings limit, retirees will have a bit more breathing room.

Tip: To maximize your Social Security benefits, use the SSA’s official calculator to plan your claiming strategy before 2026.

The Bigger Picture: Social Security in 2026 and Beyond

The 2025 Social Security Trustees Report projects that by 2033, the trust fund may be partially depleted if no reforms are made. That could mean benefit cuts of around 20% in the 2030s unless Congress acts. However, for 2026, the system remains solid, and these incremental changes are designed to keep it that way.

Here’s what else is changing:

- Wage base for Social Security tax increases to $184,500.

- Credit earnings requirement rises to $1,760.

- Maximum benefit at FRA increases to roughly $4,030/month.

- Disability thresholds rise slightly, helping SSDI recipients.

- Spousal and survivor benefits adjust automatically to reflect COLA increases.

- Tax thresholds remain unchanged, meaning higher earners may still owe taxes on up to 85% of their benefits.

How This Affects Retirees Who Keep Working?

Many retirees are working not because they have to, but because they want to. Staying active, social, and financially independent are huge motivators. According to AARP, about 1 in 3 retirees continue to work in some capacity after claiming benefits.

Working during retirement offers more than just money:

- Keeps your mind sharp and body active.

- Boosts social connections and prevents isolation.

- Provides purpose after decades in the workforce.

The 2026 update just makes it easier to do that without financial penalties. And for employers, it’s an opportunity to retain skilled, experienced workers in industries facing labor shortages.

Step-by-Step Guide: Maximizing Social Security in 2026

Here’s a simple, practical plan for navigating these new rules:

- Check your earnings record at ssa.gov/myaccount.

- Estimate your benefits using the SSA calculator.

- Plan part-time work strategically if you’re under FRA.

- Coordinate income streams — Social Security, savings, and retirement accounts.

- Consult a tax professional to minimize taxes on benefits.

- Adjust your retirement budget based on COLA and medical costs.

- Monitor inflation and Medicare premiums — these affect real income.

- Revisit investment allocation to protect against market volatility.

Common Mistakes to Avoid

Even with good intentions, many retirees make avoidable errors. Here are the big ones:

- Claiming too early: Taking benefits before FRA can permanently reduce payments.

- Ignoring taxes: Social Security isn’t always tax-free.

- Failing to report earnings: SSA matches your reported income.

- Not updating contact info: Keep your My Social Security account current.

- Missing out on spousal or survivor benefits: Explore all options before claiming.

- Relying solely on COLA increases: Inflation can outpace annual adjustments.

Expert Insights and Professional Takeaways

Financial planners agree that the 2026 updates are a net positive for retirees. Mark Hamrick, senior economic analyst at Bankrate, notes that “flexibility in earnings allows retirees to stay engaged without worrying about losing benefits.”

Certified Financial Planner Tip: Pair part-time income with delayed claiming to build a stronger financial cushion. Use your 60s to strategically manage income and taxes.

Retirement Advisor Insight: Consider reinvesting withheld benefits or part-time earnings into Roth IRAs or low-risk ETFs for long-term growth. This ensures your money continues working for you even in retirement.

Pro Insight: Consider low-risk investments like Treasury bonds, CDs, or dividend-paying stocks to complement Social Security income.

How Much Can You Get from New York’s HEAP Program? The 2025 Payment Breakdown Explained

5 Urgent Money Moves to Make Before 2026; Build Wealth and Save Thousands Starting Jan 1

Trump Is Extending Obamacare Subsidies? Inside the Surprising Twist That’s Changing Everything